- This Week Is SIC 2026

- Shootout at the

OK CorralEccles Building - Inflation Keeps on Trucking

- A Solid Win For Muddle Through

- Quarter over Quarter GDP Growth

- What Will Warsh Do?

- Welcome Jacob Shapiro and The World Isn’t Ending

- Boston, China? And Cats

There is a lot to unwrap this week. We’re going to explore what happened at the Fed, and what changes we can expect. Let’s just say it’s not what some are predicting, at least in my humble opinion. Inflation is sadly a growing problem. And that complicates Kevin Warsh’s coming tenure as Fed chair.

There’s lots to cover. But first…

This Week Is SIC 2026

SIC starts Monday. It’s important to gather our thoughts at moments like this when the sandpile feels more unstable than usual. We don’t know which grain of sand will be the one that finally sets things in motion, or when it will happen, but the fingers of instability are clearly growing.

We’ve assembled an extraordinary faculty this year. You really do need to see who they are to get the full perspective. I’m genuinely excited to hear how they’re thinking about what comes next… and, just as importantly, how to get through it with some measure of clarity.

If you haven’t picked up your ticket yet, what are you waiting for? Over 35 speakers across five days, seven panels this year. I’d love for you to join us live. But if you miss a session or day, as always, all recordings and transcripts are included with your registration. If you haven’t looked at the agenda or speaker lineup, I urge you to do so now and reserve your spot here.

Ed D’Agostino and I literally just got off a call with Professor Tyler Cowen who will be our final speaker and then will join the final panel for the SIC. His topic is going to be “How the World Will Change in the Next 20 Years.” You really don’t want to miss that. As well as the other 35 speakers with the same amazing content we had parked 22 years. Join me.

Shootout at the OK Corral Eccles Building

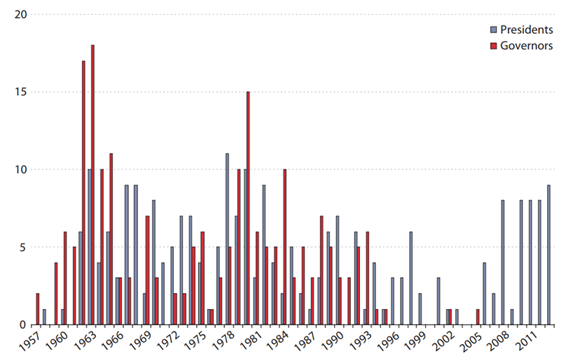

Federal Reserve Chairman Jerome Powell oversaw his “swan song” FOMC meeting this week. There were four dissenting votes. The last and only time we saw four dissenting votes was in October 1992. There have been several dozen FOMC meetings with three dissenting votes, with the most recent confirmed case occurring in September 2019. I’m looking forward to reading the minutes of that meeting, as it will set the tone for the rest of the year. At least I think it will.

While looking into this, I ran across an interesting study from the St. Louis Federal Reserve. They looked at dissenting votes from 1936 to the present, but the graph starts in 1957. I was not aware that from 1955 to the early 80s there could be anywhere from 10 to 19 FOMC meetings per year. Which is why the graph below shows more dissenting votes by year in the earlier years. Just a lot more opportunities for dissenting votes. Also note that since 2000 through 2013 the large majority of dissenting votes came from regional presidents. Except during Powell’s tenure, where two governors dissented last summer. Before that it was 1993 when both Wayne Angell and Larry Lindsey (I had the privilege of meeting both of them) dissented and wanted higher rates at a Greenspan FOMC meeting.

Source: A History of FOMC Dissents | St. Louis Fed

Why the history? Because this is the FOMC that Kevin Warsh is inheriting. Stephen Miran predictably voted for a rate cut. Three other regional presidents, while not wanting a rate hike at that meeting, did not want to include language indicating the Federal Reserve had an easing bias.

Further complicating things, Chairman Powell made it clear this week that he would not give up his Federal Reserve governor post as his term is not yet expired. Even though his term expired in January this year, Miran is staying on as governor until someone can be appointed to replace him. That someone will be Kevin Warsh. Powell is staying on ostensibly to ensure the independence of the Fed. Powell said he’d stay on as governor until “the investigation [into the cost overruns on the Fed Building] is well and truly over,” and promised “to keep a low profile” and support the new chair.

Given that the Fed Taj Mahal was started before Powell’s term, and as many government contracts was woefully underbid, it is not shocking that there were cost overruns, especially in a highly inflationary construction environment. While this might make for good theater, it does not make for good policy. In the interest of moving on quickly, the IG should officially drop the case, declare Powell not at fault, and Powell should leave. It cannot be constructive to have Powell on the board even if he does vote with Warsh. I understand what he is doing, but I don’t like it.

But that is not the biggest problem facing Warsh. His first meeting as Chair will be June 16 – 17. It is widely expected that he will cut interest rates at that point. I think you could easily get more than three dissents on that, as the macro environment is just not conducive to rate cuts, no matter what President Trump says.

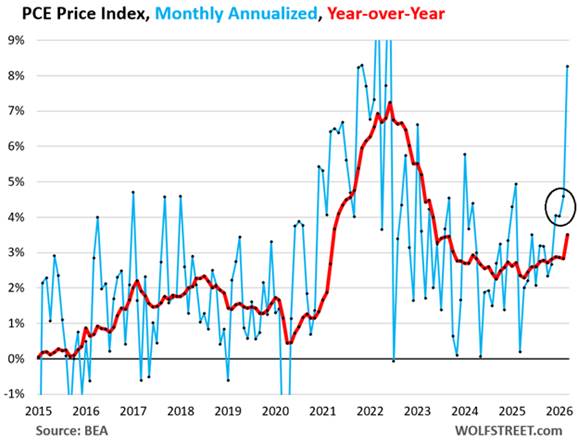

Inflation Keeps on Trucking

This is a great summary of the inflation data from the PCE inflation index, the Fed’s favorite measure. From Wolf Richter:

“The PCE price index, which the Fed favors for its inflation yardstick, spiked by 0.66% in March from February (+8.3% annualized), the worst spike since mid-2022 at the peak of the inflation surge.

“Inflation has been accelerating since mid-2025. In each of the three months of December, January, and February – so before the war and before the energy price spike – the PCE price index had already surged by 4% to 4.6% annualized (black circle in the chart). The March spike is on top of that acceleration (blue line). And it was energy, but not just energy.

“Year-over-year, the PCE price index jumped by 3.5%, the worst since May 2023 (red line). The Fed’s target for the year-over-year measure is 2.0%, and PCE inflation has been moving away from it relentlessly for the past 10 months, and the energy price spike came on top of it.”

While a lot of it was energy, inflation was widespread throughout the economy. Core services jumped almost 4% annualized and has been rising since August of last year. Durable goods are rising by more than 5%. This is a long way from the Fed’s target of 2%.

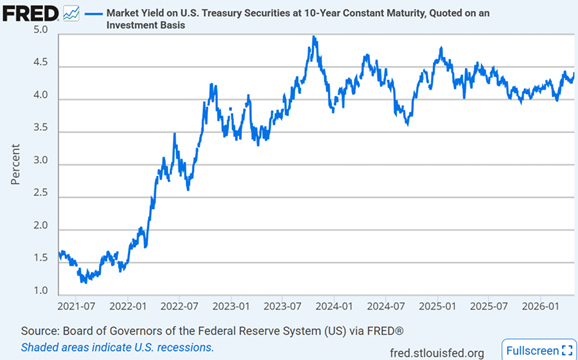

Six months ago the ten-year yield was the 3.98%. It’s been somewhat higher and a lot lower over the last five years. The ten-year, to a significant degree, reflects the inflation expectation outlook. Lowering the Federal Reserve rates without lower inflation will not reduce the mortgage rate, no matter how much we would like it to. In fact, it might have the perverse effect of making the bond market believe that the Federal Reserve is not serious about inflation.

This disconnect between the central banks short-term rates and ten-year notes is not just a US phenomenon. As the US ten-year yield is touching 4.40%, the ten-year JGB yield closed overnight at a 29 yr high, the German ten-year yield is at a 15 year high, and the ten-year UK yield is at an 18 yr high. Debts and deficits matter too. (H/t Peter Boovkvar)

A Solid Win For Muddle Through

Further complicating the case for a rate cut is the economy. It just keeps truckin’ on, as the Grateful Dead song said. Annualized GDP for the first quarter was 2%. But the year-over-year rate was 2.7% growth in GDP.

Quarter over Quarter GDP Growth

Note in the chart below the extreme swings in GDP growth since January 2025. The 1st quarter 2025 was impacted by front running tariffs (imports are negative for GDP). Then the large rebound as things balanced. The weaker 0.5% growth of the fourth quarter 2025 was almost entirely due to the government shutdown, and part of the 2% growth for the first quarter of 2026 was catch-up from the government shutdown.

For the year ended March 31, 2026 the year-over-year GDP growth was 2.7%. Given all the uncertainties, that is a solid number. 2.7% annual growth does not exactly scream for more rate cuts. If you simply look at real final sales to private domestic purchasers, which Powell especially, and the Fed in general, like to talk about, annualized GDP for the quarter would have been 2.5%. Yes, somewhere around half of GDP growth was in AI data center construction. But in almost every period of history there is always something that is a main driver. I suspect we will be talking about how robots are the main driver for GDP somewhere in the 2030s. It’s always something…

Source: United States GDP Growth Rate

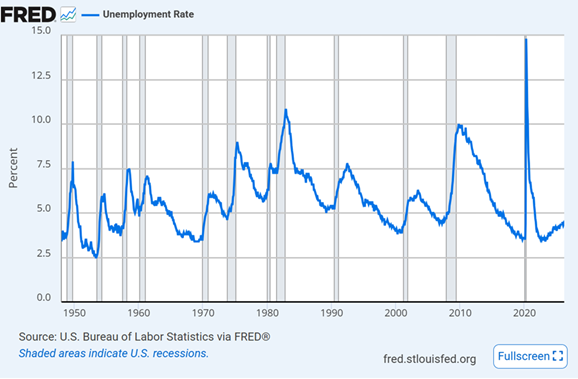

Unemployment is solid at a reasonably low 4.4%. We touched on this last week. Part of the reason is the 2.5 million illegal immigrants who have either voluntarily or forcibly been returned to their home countries. To get a historical perspective on how good this number is, look at this graph of the last 75 years. There has only been one time in the last 50 years when unemployment was lower. It is hard to make a case for rate cuts with low unemployment. Yes, I know, job openings are decreasing and turnover is less, but 4.4% is still a solid number.

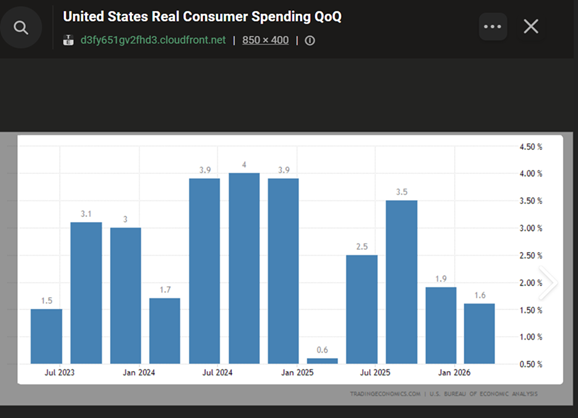

Consumer spending slowed to 1.6% real growth despite high inflation. But as you can see from the chart below, periods of lower consumer spending are generally followed by higher spending. It is seemingly in the American DNA to keep on consuming. Again, nothing in this data suggests the need for a rate cut.

Source: United States Consumer Spending

What Will Warsh Do?

Kevin Warsh has a dilemma. President Trump expects a rate cut. The data doesn’t call for one. Then again, one rate cut of 25 basis points will not put us into an inflationary spiral, especially if the accompanying statement talks about the need to be vigilant about inflation.

The market is assuming Warsh will not cut rates. That would be consistent with his speeches and interviews. I hope that’s the case. I truly believe Kevin will be the adult in the room. Because we don’t have any adults in the leadership of Congress trying to bring down the budget deficit.

Let’s be clear, right now it is fiscal policy that is driving inflation and not Federal Reserve policy. The longer we run $2 trillion deficits (even though it has come down some) the market is not going to assume inflation is under control. US government debt to GDP is now 122%. Total US national debt will go over $40 trillion this year. Interest on the debt is slightly over $1 trillion. My friend Niall Ferguson points out that empires do not last when their interest costs are higher than their defense spending. We are there.

Chairman Warsh is committed to reducing the balance sheet and wants to streamline the bureaucracy at the Fed. Both are excellent goals. I believe he understands that inflation is job number one. I would expect that sometime this year he will begin to talk about the need for containing the growth in debt and more fiscal responsibility. My simplistic analysis is that we are entering a period where monetary policy will no longer work as it has in the past. Just as we are seeing long-term rates rise around the world because of fiscal profligacy, the same will happen in the US. The real limiting factor on US growth is not Federal Reserve policy but out-of-control spending and the bipartisan congressional commitment to spending growth.

At some point the bond market will simply indicate to Congress that they have to make changes in the way they do business. Otherwise long-term rates are going to continue to go up no matter what happens with short-term rates. We squandered a generational opportunity to sell 30-year bonds at 2% five years ago, and I doubt that will ever happen again. But that would have just delayed the inevitable, as the long-term debt will be $50 trillion plus in 2030. Interest-rate expense will be in the $1.5 trillion plus range. It will get interesting. Which is just another reason why you need to sign up for the SIC.

How are you going to handle your own borrowing and expenses, let alone capital investments? Debt is future consumption pulled forward, which means there will be less consumption in the future as we use that money to pay back the debt. Stay tuned…

Welcome Jacob Shapiro and The World Isn’t Ending

I have long been a fan of geopolitical analyst Jacob Shapiro. I am excited to announce that he has joined the Mauldin Economics team and will write a free letter called The World Isn’t Ending. The point being that all the headlines want to make every geopolitical event the trigger for the apocalypse, or even Ragnarok. And it never is. That doesn’t mean geopolitics isn’t important, because it is. It affects how we invest and live.

But if your analytical style is to run around with your hair on fire talking about how the sky is falling, then you are doing your readers and listeners a disservice.

Jacob’s inaugural letter is entitled “Hormuz: The $200 Crude Question.”Here are his first few paragraphs:

“The World Isn’t Ending opens mid-conflict, as the US-Israel ‘military operation’ against Iran drags on despite Trump’s repeated promises that it will end “very soon.”

“Humans have an evolutionary penchant for focusing on the negative, and our newsfeeds and algorithms feed that. But I am here to say, it is in many ways the best of times, and that controversial lens defines this letter.

“My mission here is to describe the world as it is, not as I would wish it to be—and to do so without being boring. I want to challenge you to think differently about the world, using the tools of geopolitical analysis to your advantage. I’m grateful you’re along for the ride.

“With that, let’s discuss the war because the simple truth is that nothing happening in the world is as important.”

You can read that letter and his analysis here. It’s a short and fun read and you will learn a lot. Look for Jacob in your inbox every Thursday.

Speaking of which, this cartoon hit my inbox as I was writing. Sent by my friend Stephen Moore, this seems an appropriate end to this week’s letter.

Boston, China? And Cats

I am heavy in preparation for the SIC along with everything else. I have no plans to travel in May but that will likely change. I will be going to Boston the first week of June and then Shane and I are actively trying to figure out how to get to China the last week of June. I have never been and really would like to go.

Those of you who read Jared Dillian know that he has a house full of cats. I am basically allergic to cats and so my poor wife Shane had to give up her cats when she moved in with me. She was really attached to her cats and animals. When we moved in Dorado, we inherited two more or less feral black cats who lived outside. Shane fed them and kept them and they were her cats and she was happy. Then sadly, one of them was no longer with us and that really depressed her. She spent over a month looking for that cat.

A few months ago, she came into my room and showed me a list of 10 different breeds of cats that are hypoallergenic. “John, these cats won’t trigger your allergies. Can we get one?” The look in her eyes told me I needed to pay attention to this. So, I looked at the various breeds, most of which were fairly ugly (at least in my opinion) but they had one breed called a Russian Blue which I like, so I agreed to get one with the provision that if I end up being allergic we would give it away.

A week later, she told me the breeder says these are very social animals and we should get two. Call me weak willed, but I challenge you to look in those eyes and say no. So now we have two 6-month old kittens. My allergies haven’t kicked in any more than normal for Puerto Rico, so another month or so I may even allow them into my lap. I will admit they are quite cute and fun to watch as they play. My wife boosted the GDP by buying every cat toy known to man.

For those of you know my son Trey, he just had his first daughter this week, which makes for 13 grandchildren. As far as I know I’m thankfully not allergic to grandchildren.

And with that, I will hit the send button. You have a great week and I’m hoping you join me at the SIC. As I’ll be fairly busy with the conference next week, we will have a very special guest writer for next week’s letter. And don’t forget to follow me on X as I will be posting off and on during the week.

Your staying calm and carrying on analyst,

John Mauldin

Co-Founder, Mauldin Economics

Read the full article here