Gold has an inverse relationship with US Treasury yields. As yields rise, gold normally falls, as interest-bearing assets become more attractive compared to gold, which offers neither interest nor a dividend.

The opposite happens when yields fall, normally.

Like gold, Treasuries are a haven during geopolitical crises like the current war in the Middle East.

But Treasury yields are climbing sharply as geopolitical tensions, a $1.9 trillion deficit, and waning foreign demand undermine their safe-haven status. China is selling Treasuries at rates unseen since 2008.

(Rising yields means less demand for Treasuries, because prices and yields move in opposite directions.)

Source: Trading Economics

Source: Trading Economics

Divided Fed

The US central bank recently kept its benchmark interest rate unchanged within a range of 3.5 to 3.75%. The market is watching closely to see whether the Fed shifts to a monetary easing policy (lower rates), which are generally good for equities.

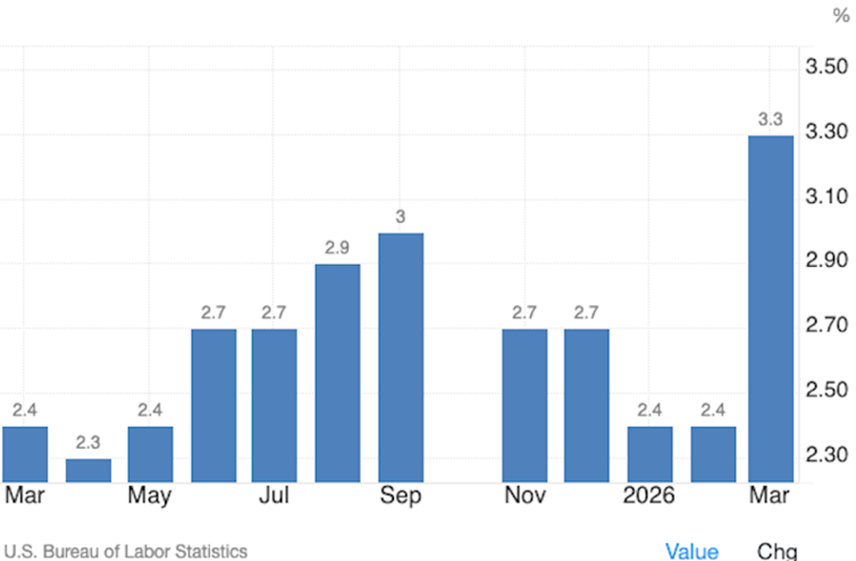

Last Wednesday, the day of the Fed decision, traders were betting there would be no rate cut in 2026 after oil prices jumped. Higher oil prices feed into inflation fears. US inflation in March rose to 3.3%, year on year, a significant climb from January and February’s 2.4%.

One source says US consumer inflation, the CPI, “is rapidly coming into view.”

US inflation. Source: Trading Economics

The last thing the Fed would do in an inflationary environment is cut interest rates, since this results in consumers and businesses spending more, which drives prices even higher.

When US inflation reached a 40-year peak of 9.1% in June 2022, the Fed hiked its Federal Funds Rate 1.5% to 1.75%, the largest increase since 1994.

The direction of interest rates is causing dissension among the Federal Reserve’s board of governors. The April 29 decision was reportedly the most divided since 1992, with eight officials voting to hold the FFR in the range of 3.5-3.75% and four dissenting — three who took issue with the Fed’s bias toward easing rates and one who voted to cut rates.

Why does the Federal Reserve have a bias toward easing? According to CNN, the word that most troubled the dissenters in the Fed’s lengthy policy statement released last week was “additional”:

On Wednesday, its latest forward guidance hinted that lower interest rates might be the only possibility moving forward, noting it will consider “additional adjustments to the target range for the federal funds rate…”

The word “additional” specifically drew objections. Fed presidents Lorie Logan of Dallas, Beth Hammack of Cleveland and Neel Kashkari of Minneapolis “did not support inclusion of an easing bias in the statement at this time…”

Since 2024, the only adjustments the Fed has made to the target range have been down, largely driven by signs of a weakening economy. But the economic situation has dramatically changed this year: The US-Israeli war with Iran, which began on February 28, has kept global oil prices hovering around $100 a gallon for weeks and has kept US gas prices elevated…

Fed watchers interpreted the use of “additional” in the policy statement as evidence of “easing bias,” or that officials are leaning toward lowering rates in the near term, while signaling that rate hikes are not likely…

Kevin Warsh, President Donald Trump’s pick to lead the Fed, is on track to take the reins in just a few weeks, and Warsh may push for lower rates, since he was nominated by a president who has long pounded the table for rate cuts. That’s also drumming up the perception that the Fed is leaning toward lowering rates, which the three Fed presidents who dissented are firmly against…

Hammack’s statement explained that “this clear easing bias” is “no longer appropriate given the outlook” because not only is the Iran war stoking inflation pressures, but the US labor market seems to have stabilized, meaning there’s no urgency to deliver rate cuts to stimulate the economy.

The bottom line? It looks like the Fed is not going to lower rates in 2026, which will be negative for gold. Even if the new Fed Chair Kevin Warsh tries to lower rates, what happened last week indicates he will face opposition from the other board members.

FX Street states a higher-for-longer US rate stance amid inflationary pressure could undermine the gold price.

Stagflation

But not if current events lead to stagflation, when the inflation rate is high, economic growth rate slows, and unemployment remains steadily high. (Corporate Finance Institute)

In the 1970s, when the US was hit with two energy crises — the OPEC oil embargo and the Iranian Revolution — gold experienced a massive and historic bull market, rising from a fixed $35/oz to a peak near $850/oz by January 1980, an increase of over 2,300%.

As we’ve previously written, gold does well in stagflationary periods and outperforms equities during recessions.

In six of the last eight recessions, gold outperformed the S&P 500 by 37% on average.

Capital Economics says a useful rule of thumb is that a 5% rise in oil prices adds about 0.1% to developed-market inflation.

High oil prices also dampen economic growth, with the IMF estimating that for every 10% rise in oil prices, global economic output decreases by 0.1 to 0.2%.

Oil price increases not only contributed to the twin energy crises of the 1970s, but the US recessions in 1990 and 2008. Russia’s invasion of Ukraine in February 2022 also triggered a major energy shock, particularly in Europe.

As of this writing, Brent crude was trading at $110.46 a barrel.

Source: Trading Economics

Source: Trading Economics

The United States is not immune to stagflation and was looking vulnerable even before the war started.

The economy lost 92,000 jobs in February, while the unemployment rate ticked up to 4.4%. In March it was 4.3%.

For manufacturing the job losses are terrible. The sector in February was down to 12.57 million jobs, the lowest since January 2022.

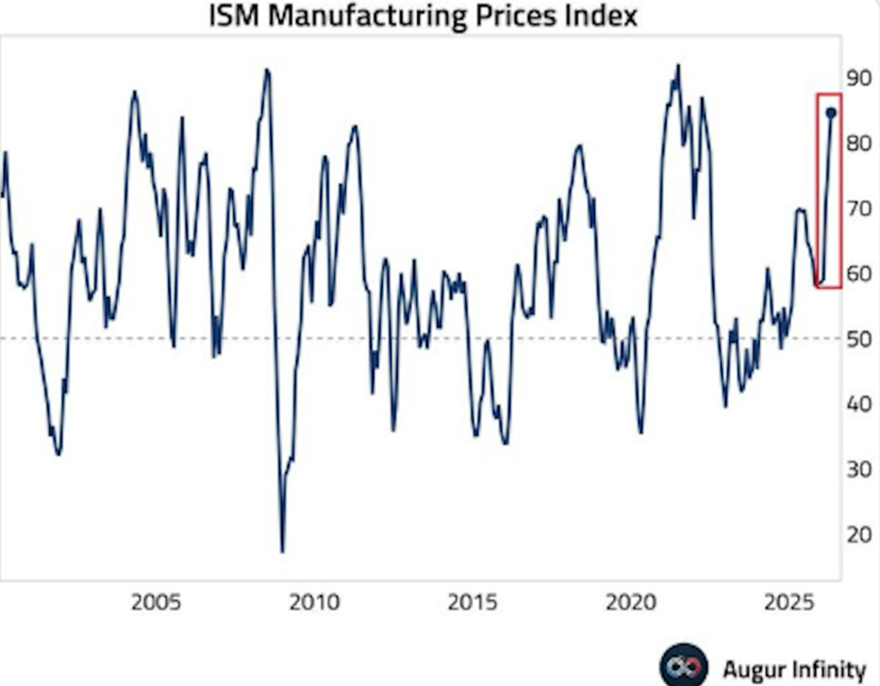

According to the Kobeissi Letter, stagflation is intensifying across US manufacturing. Although the ISM Manufacturing PMI was steady in April at 52.7 (anything above 50 signals growth), the ISM Manufacturing Prices Index surged 6.3 points to 84.6, the highest since May 2022.

Source: X

Source: X

In fact, prices paid have risen 25.6 points over the last three months, which is the biggest three-month increase on record.

“The surge continues to be driven by surging steel and aluminum prices affecting the entire supply chain, tariffs on imported goods, and higher energy and materials costs driven by the Iran War. Meanwhile, the employment index fell -2.3 points, to 46.4, the lowest since January, marking the 15th consecutive monthly contraction. Stagflation pressures are building again.”

The Iran war and stagflation — Richard Mills

An article by Dow Jones cites Citi analysts saying that defensive sectors will outperform if oil price gains are sustained.

Citi’s team of quantitative analysts has studied the market and says it’s beginning to smell like stagflation…

So where are we right now? Based on a 22-day rolling correlation of market returns, the strategists say the market is moving from a more benign recovery/normal regime early in the year “toward a regime that looks much more like inflation boom and tighter financial conditions, i.e. the typical regime we see prior to stagflation.”

Gold and real yields

Several factors influence gold prices (mainly the US dollar, gold ETF inflows/ outflows, inflation rate, bond yields, safe haven demand, physical gold demand, gold supply) but none is more reliable than real interest rates.

Real interest rates and gold — Richard Mills

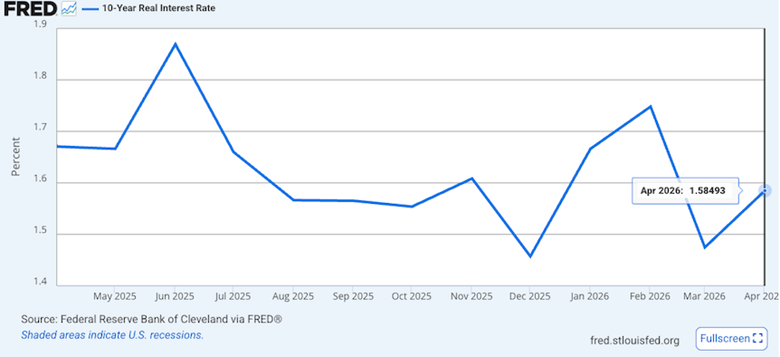

The reason for this is simple. When real interest rates (interest rate minus inflation) are low, at or below zero, cash and bonds fall out of favor because the real return is lower than inflation. If you are earning 1.6% on your money from a government bond, but inflation is running 2.7%, the real rate you are earning is negative 1.1% — an investor is actually losing purchasing power. Gold is the most proven investment to offer a return greater than inflation, by its rising price, or at least not a loss of purchasing power.

The current real interest rate is +1.1% (4.4% – 3.3%). The fact that real interest rates are positive goes some way to explaining why the gold price is falling despite a war in the Middle East and rising inflation.

Source: FRED

Source: FRED

An article written last Wednesday, April 30th, the day of the Fed decision, agrees that real yields are doing the damage to gold.

“When risk-free paper pays north of 4% and the Fed signals patience, a non-yielding asset like gold loses its edge fast,” writes Yahoo Finance.

Indeed, the spot gold price is down 22% since hitting an all-time high of $5,594.80/oz in early February, at time of writing Tuesday morning.

Source: Trading Economics

Source: Trading Economics

Yahoo Finance notes the gold price and gold ETFs like GLD are losing ground to equities. In the month prior to April 30, the S&P 500 (SPY) climbed 12% and the VIX volatility index fell to 18, “signaling capital rotation from defensive trades.”

Source: Yahoo Finance

Source: Yahoo Finance

But could this be a blip? The article reminds that GLD is still up 36% over the past and 6% year to date, “so the broader uptrend is intact.”

Central bank de-dollarization

Last year, central bank gold reserves surpassed US Treasury reserve holdings, marking the first time this has happened since 1996.

Since the 2008 financial crisis, central banks worldwide have added over 225 million ounces to their gold reserves, while the US dollar’s share of global reserves has fallen from over 60% in the early 2000s to around 40% today.

In each of the last three years, central banks have collectively purchased over 1,000 tonnes of gold — double the annual average from the previous decade.

Reasons for such high levels of central bank buying include post-pandemic inflation eroding confidence in the purchasing power of fiat currencies; the deterioration of US fiscal health — rising deficits are causing investors to worry about the country’s ability to manage its debt; gold is a neutral asset to settle transactions between nations, with no counterparty risk; Treasuries are vulnerable to sanctions; and gold has traditionally outperformed sovereign bonds and currencies during military conflicts and financial crises.

According to Investing Live, Central bank buying has been the dominant driver of gold demand since 2008, and the broadening of that buying beyond the major accumulators to include Saudi Arabia, Qatar, the UAE and Egypt suggests the trend has further to run.

$8,000 gold?

Deutsche Bank last week published a scenario analysis projecting gold could climb as high as $8,000 within five years if central banks were to increase their gold allocation to 40% of reserves from the current 30%.

The conceptual projection is grounded in the bank’s assessment of de-dollarization trends among emerging central banks.

With gold making up just 16% of emerging central bank reserves, the site says gold has significant headroom if those institutions move toward a 40% target allocation.

16% is a remarkably low figure given that they have accounted for all net central bank gold purchases since the financial crisis.

Deutsche Bank’s structural case for prices approaching $8,000 is “anchored in one of the most significant shifts in global reserve management in a generation”:

Deutsche Bank’s explanation for why this is happening draws on a broad geopolitical thesis. The post-Cold War era, built on US-led multilateralism, free trade and dollar dominance, is unwinding. The US is retreating from its traditional role as guarantor of global security and open commerce, and the weaponization of the dollar banking system through sanctions has given emerging market central banks a concrete operational reason to diversify away from dollar assets. Gold is the natural beneficiary of that shift: it is liquid, universally accepted and carries no sovereign risk, as it is not the liability of any government or central bank.

The Yahoo Finance article says JPMorgan and Wells Fargo are in the same camp, pegging year-end targets in the $6,000 to $6,300 range, a growing Wall Street consensus that gold’s ascent is far from over.

World Gold Council report

Before falling back on our bullish gold forecast, we should check with the World Gold Council, which closely tracks the precious metal’s demand and supply trends.

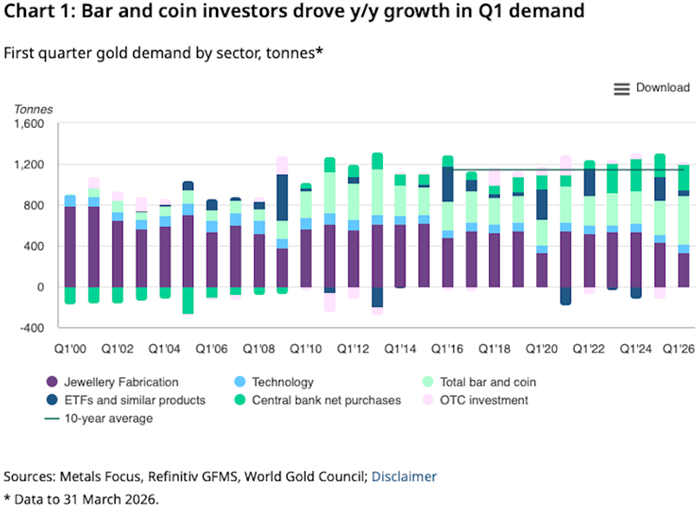

WGC’s latest report, published April 29, says that bar and coin buying drove first-quarter demand, which was 2% higher year on year at 1,231 tonnes.

Source: World Gold Council

Source: World Gold Council

Other key findings:

- Bar and coin demand of 474t (+42%) was the second highest quarter on record. Asian investors led the charge, hoovering up gold investment products.

- Buying of gold-backed ETFs continued in Q1 (+62t), but at a lower rate than the very strong Q1’25 (+230t) following sizable outflows from US funds in March.

- Central banks bought 244t (+3% y/y) of gold on a net basis in Q1 despite a visible uptick in selling activity during the quarter.

- Demand for gold used in technology edged 1% higher to 82t, fuelled largely by the continued growth in AI infrastructure.

Peak gold

We note that global gold demand continues to outstrip mine supply; demand cannot be satisfied without gold recycling. Mine production of 884.7t in Q1 2026 failed to meet quarterly demand of 1,231t without recycling 366t. This is our definition of peak gold.

Peak gold — Richard Mills

A US-focused Q1 WGC report from the same date states that, Despite near‑term volatility, ongoing geopolitical tensions, policy‑rate uncertainty and broader macroeconomic risks continue to support the longer‑term investment case for gold in the US.

Conclusion

While 2025 saw record gold production, mining faces a potential cliff this year as the pipeline of large-scale projects shrinks.

Causes of the mined deficit includes dwindling reserves, a lack of new discoveries, declining ore quality, and resource nationalism.

Identified, economic gold reserves are estimated at only about 20 years’ worth of mining at current production rates (approx. 59,000 tonnes remaining), states The Oregon Group.

The industry is increasingly relying on junior explorers to fill the gap in finding new deposits. However, the long-term trend points towards a sustained tightening of gold supply due to geological scarcity and the long lead times required to bring new mines into production.

Beyond these operational challenges, the gold bull market is considered to be intact, with structural drivers such as persistent central bank accumulation, geopolitical risk, and monetary debasement fears supporting a multi-year uptrend despite early 2026 volatility.

The market is starting to price in stagflation. Real assets such as real estate, gold and commodities are being repriced for persistent inflation, manufacturing slowdown, slowing global growth and rising unemployment. Quant analysts have noted that return patterns in early 2026 mimic previous stagflationary regimes, with simultaneous underperformance in both equities and bonds.

Real estate is being valued for its ability to provide income while acting as a partial inflation hedge.

Despite economic concerns, demand for hard assets persists due to high replacement costs and supply chain constraints.

Gold is viewed as a key hedge against monetary instability.

The Manufacturing PMI has shown signs of softening, with employment in the sector edging down, particularly in Canada, where manufacturing employment dropped by roughly 52,000 year-over-year by March 2026.

Job markets are beginning to show weakness. Although some stabilization has occurred, layoffs have increased in specific sectors.

Central banks, such as the Federal Reserve and the Bank of Canada, are facing a “difficult balancing act,” where maintaining high rates to fight inflation risks further weakening the labor market.

At AOTH we believe markets are shifting from a “Goldilocks” scenario (low inflation, high growth) to bracing for stagflation, where defensive, tangible assets are expected to outperform.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Read the full article here