The US-Israeli campaign against Iran is remaking the Middle East. And a casualty is Dubai’s positioning as the Switzerland of the Gulf—a stable intermediary that allows capital, goods, and information to move when politics gets in the way.

In stable, unipolar moments, those kinds of intermediaries fade into the background; in fragmented, multipolar ones, they become indispensable.

Dubai looked like the model modern intermediary, a flexible, non-aligned hub optimized for a world of competing powers. So, what went wrong (apart from the obvious)? And what will replace it?

The Situation:

To understand what’s happening, a little history helps. For as long as there has been globalization, there has been a need for financial intermediaries.

It wasn’t always so.

Globalization’s first emergence was a product of creative destruction. Genghis Khan’s 13th century invasions of Eurasia disrupted power balances, leaving behind fragmented global power centers linked by ironically stable trade routes.

Source: World History Encyclopedia

That fragmentation enabled the rise of the OG global financial intermediaries: the Italian commercial republics: Florence, Venice, and Genoa. Their opulent and obviously decaying wealth today is an echo of their past importance. These were trailblazers in combining cross-border finance, banking, and legal norms that allow strangers to transact at scale.

Source: The Renaissance

Their biggest advantage was… geography. They sat at the intersection of trade between the Christian and Muslim worlds, financing commerce (and even war) across sovereign boundaries.

Geography giveth and geography taketh away. The rise of a strong Ottoman polity, the decline of the Mongols, and the European Age of Discovery saw globalization go truly global as Europeans bypassed overland trade routes. Amsterdam rose and fell as a global financial intermediary; then rose the British Empire and its imperial nodes (Bombay, Alexandria, Singapore, Hong Kong).

As the sun set on the British Empire, the world turned “multipolar” once more. That fractious environment led to World Wars I and II, wars that seemed unthinkable to the wealthy and powerful during La Belle Epoque, when globalization seemed inevitable and fundamentally good. It also led to the rise of Switzerland as a different kind of global financial intermediary, a safe haven for capital when the global stage was too volatile.

Switzerland and Singapore today are the gold-standard safe-haven cloisters: legally reliable, politically neutral, geographically removed from conflict, and trusted by global capital.

The Gulf’s Unlikely Switzerland

In the again-multipolar world—with its sanctions, tariffs, regulatory divergence—there is demand for optionality. Capital asks: Where can I go that isn’t fully subject to Washington, Beijing, or Brussels? In recent years, a popular answer was “Dubai.”

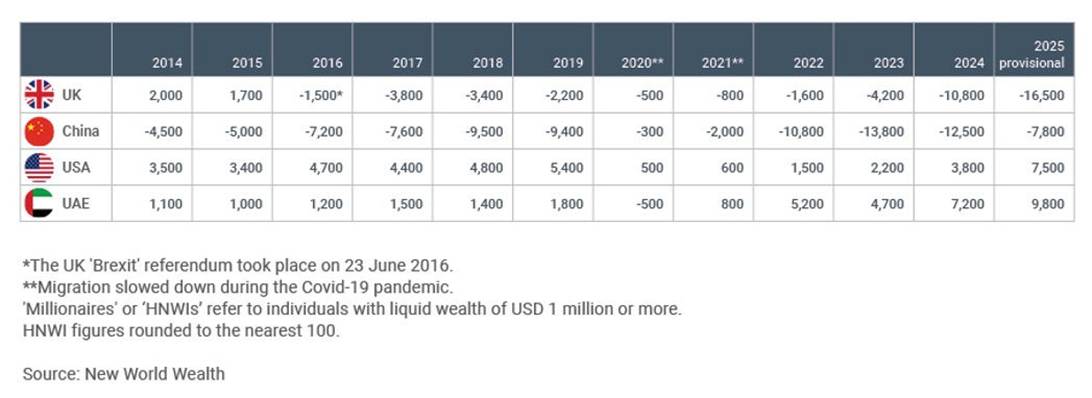

In under half a century, the United Arab Emirates reinvented itself from a British-protected petro-kingdom into a modern economy with real diversification and outsized regional influence. GDP more than quadrupled in 20 years; GDP per capita nearly doubled. In 2025 alone, the UAE saw a net inflow of 9,800 millionaires with a collective investable wealth of ~$63 billion.

Source: New World Wealth

Here’s the rub: It’s over.

Yes, that’s melodramatic. The UAE will likely still function as a tax avoidance haven for Russian oligarchs or wealthy Indian industrialists. But its success over the last 20 years is a casualty of the US-Israeli campaign against Iran. The UAE will be like the cantina in the space port of Mos Eisley in A New Hope.

Moreover, the war is simply the nail in the coffin. For the last ~10 years, the UAE has been busy disqualifying its own success:

- It was never going to achieve geographic distance from zones of conflict.

- It has not disconnected itself from the US—the AED is pegged to the dollar.

- It is leveraging its sovereign wealth to fund massive, high-risk projects tied to AI and technology in the US, to the profligate tune of almost $2 trillion.

Add to that, the UAE government is active in conflicts in Yemen, Ethiopia, and Sudan, pursuing imperial ambition rather than protecting and extending what made it attractive to capital (a Venetian error).

In fact, the UAE has botched strategic neutrality so badly that it has been the target of more Iranian missiles and rockets than Israel.

There is useful historical precedent. Lebanon was once on the path to becoming the Switzerland of the region. From an October 23, 1964 edition of Time Magazine:

Lying fat and silky beneath the Mediterranean sun, Beirut is an oasis of prosperity in the Arab Middle East. Tiny Lebanon’s flamboyant capital sprouts new buildings like palm trees, boasts more Mercedeses than mullahs, lures thousands of tourists and happily shares its year-round sunshine with courtesans in bikinis as well as desert Arabs in burnooses. But Beirut’s most beneficent climate is the climate of trade, the heritage of its Phoenician forebears. In the Levantine landscape nothing seems to grow faster or greener than the city’s banks. Beirut is the world’s newest and fastest-rising financial center. In the last decade it has expanded its banking business by 1,000%—and it shows no signs of slowing.

Spoiler alert: Lebanon was done within a decade, consumed by civil war and eventually an Israeli invasion. It never truly recovered and is in decline now. And Lebanon is a beautiful country. It is not a petro-kingdom in the middle of the desert.

Perhaps the negativity is unwarranted. Perhaps the US will crush Iran, or perhaps regime change will throw down the Ayatollahs. But the geopolitics is clear. It is not on the UAE’s—or any Gulf country’s—side.

Where to Next?

Still… the world isn’t ending. The UAE success story will be replicated elsewhere. After all, the UAE had the right idea—open to multiple blocs, politically flexible, optimized for moving and parking capital—but it fumbled the policy; and due to its inherent geographic disadvantages, it did not have room for error. Switzerland and Singapore are obvious winners of the fallout. But for some other countries, an opportunity has emerged.

In order of speculativeness, a few contenders:

- Uruguay already plays a similar role at a regional level.

- El Salvador lacks a long track record of stability, but the Bukele government has dramatically improved security. Its bet on Bitcoin is an attempt to create distance from the dollar system, and its geography offers an interesting mix of advantages.

- Guyana discovered a “fairy tale” discovery of oil in the 2010s that is coming online.

- Scotland would need London’s permission (unlikely)… but has some of these attributes.

These sound out there… but so would the notion of the UAE 50 years ago, and so would the notion of Singapore 200 years ago, and so would the notion of Venice in 1200.

The key is to focus on where political flexibility, legal infrastructure, openness to capital flows, and geographic positioning combine. The Mongols destroyed the world but created the opportunity for Venice. The US and Israel have destroyed what remained of the Persian Gulf’s tenuous balance of power since Gulf War 2.0, and with it the UAE’s promise.

What will it create?

Map/chart of the week:

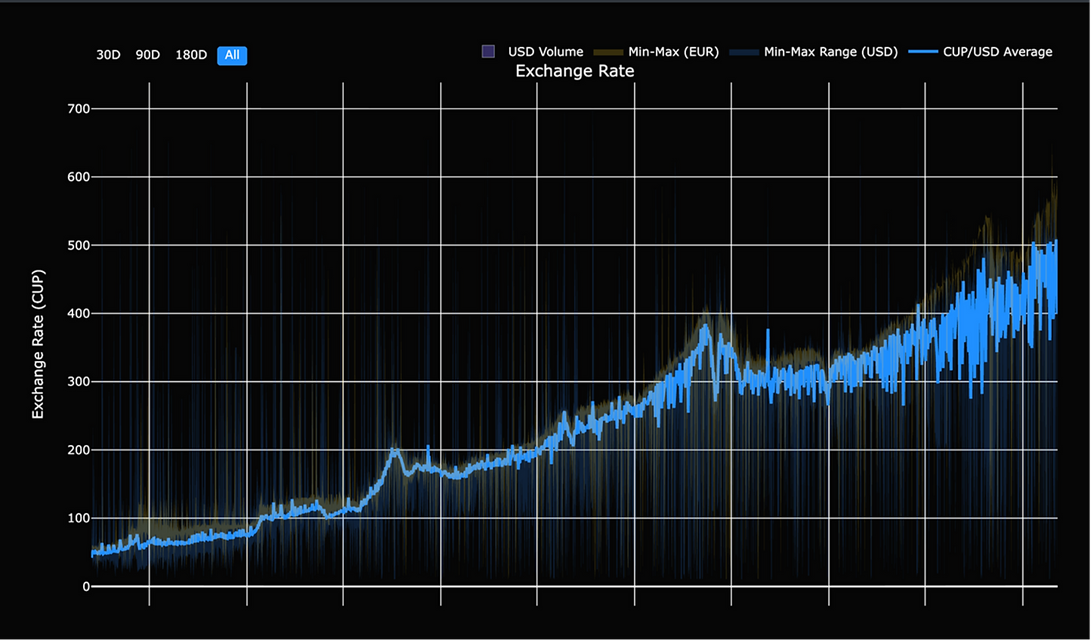

It is clear where the White House wants to go next: Cuba, which has suffered repeated nationwide grid collapses under the US oil blockade. Here’s a chart of the Cuban peso on the dollar—inflation not looking good.

Source: DevTech

Blind Spot:

Between March and May 2026, the Trump administration’s trade office quietly opened three Section 301 investigations against Vietnam. Section 301 is the legal mechanism the US uses to authorize tariffs. The first, opened March 11, targets countries (Vietnam included) accused of running excess manufacturing capacity to dump goods into the US market. The second, opened March 12, covers alleged failures to block forced-labor goods at the border. The third, opened May 29, follows the United States Trade Representative’s (USTR) April 30 Special 301 Report, which designated Vietnam a “Priority Foreign Country,” the highest tier of IP concern. USTR hasn’t applied that label to any country in 13 years, and Vietnam is the only country carrying it in 2026. Public comments on the third investigation are due July 2.

Why is this happening? Vietnam has been one of the biggest winners of US-China trade tensions—many American companies have looked to Vietnam as a place to relocate manufacturing that was once in China. The Trump administration doesn’t like that; it believes that investment and those jobs should come back to the US. Leaving aside whether that is realistic or not, Vietnam became a major topic of concern for the White House toward the end of the first Trump administration, which accused Vietnam of currency manipulation shortly before the Biden administration was sworn in.

Even more problematic, though, are the deeper ties between Vietnam and China. Vietnam’s government is also Communist in form, and its relatively new leader, To Lam, is doing his best Xi Jinping impersonation in eliminating political opposition. Moreover, Vietnam has become to China what Mexico is to the US. How do you say, “maquiladoras” in Vietnamese, one wonders? Vietnam doesn’t make the chips, the motors, the modules, the zippers, and many other components in what it produces. China does and ships them across the border to Vietnamese assembly plants.

The July 2025 Vietnam tariff deal acknowledged this by setting a 20% rate on Vietnamese-made goods and a 40% rate on “transshipped” Chinese goods routed through Vietnam, but it never defined what counts as transshipment. Trade lawyers expect US enforcement to use a near-zero tolerance test. A single Chinese-sourced part inside an otherwise Vietnam-assembled product could trigger the 40% rate.

And ironically, this is where the Vietnam story becomes part of the United States-Mexico-Canada Agreement (USMCA) review now formally underway. One of the administration’s stated objectives is to tighten USMCA rules of origin so that products with Chinese content can no longer qualify for duty-free entry through Mexico. A computer with Chinese components, assembled into a Vietnamese sub-system, completed in Mexico, currently enters the US duty-free. Washington is building legal infrastructure to break that supply chain.

The virtues of reshoring are beyond my scope—it is my remit to point out that virtuous or not, this sort of policy, if successful, will mean higher prices for goods made in Vietnam.

Reader Question:

Finally…

I’m watching: NBA Finals

I’m reading: How to Read a Book, Adler and Van Doren

I’m listening to: Hamilton soundtrack (family road trip!)

Jacob Shapiro

Read the full article here