The Federal government took in a record amount of tariff revenue in October. It also ran the highest October budget deficit on record.

The Trump administration spent $284.35 billion more than it took in to kick off fiscal 2026. That was about 10 percent higher than last year’s October deficit and about $200 million more than the previous October record set in 2020 during the pandemic lockdown era.

The deficit was inflated by the shifting of some November benefit payments back into October. If we factor out those calendar effects, the deficit would have been $180 billion. While a 29 percent reduction from last year’s October deficit, it would still rank in the top four highest October shortfalls on record.

Keep in mind that Uncle Sam ran this massive deficit while the government was “closed.” A Treasury Department official told Reuters that it was unclear how much spending was reduced by the government shutdown, but estimated it was less than five percent of total outlays.

Salaries and other outstanding obligations that were not paid during the shutdown are now due, as the government is fully operational again. That means we could see a spike in spending in November.

Houston: We Have a (Spending) Problem

The federal government took in $404 billion in October. That was a healthy 24 percent revenue increase from October 2024.

Record monthly tariff receipts totaled $31.4 billion. That was a 330.1 percent increase in customs receipts compared to October 2025.

It should be clear that claims that the federal government is going to use tariff revenue to pay a “dividend” to poor and middle-class taxpayers and pay down the national debt are nothing but political rhetoric. Math is the great enemy of this ambitious plan.

Last year, the U.S. government ran the fourth-largest budget deficit on record despite a 142 percent increase in tariff revenue.

It should also be clear that the U.S. government doesn’t have a revenue problem. It has a spending problem.

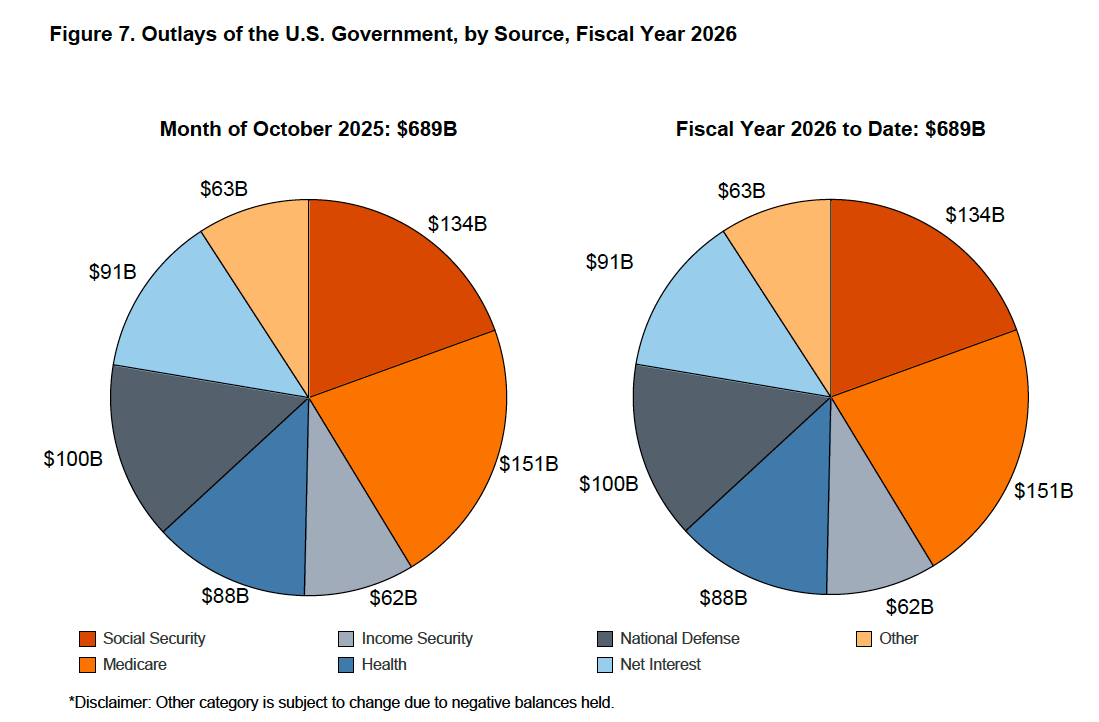

The Trump administration blew through $688.72 billion last month. That represents a 17.9 percent year-on-year increase. Last year, despite all the hype about DOGE and some lip service to cutting spending during the early days of the Trump administration, the U.S. government spent just over $7 trillion last year. That’s an average of $583.3 billion per month or $19.2 billion per day.

Last year, despite all the hype about DOGE and some lip service to cutting spending during the early days of the Trump administration, the U.S. government spent just over $7 trillion last year. That’s an average of $583.3 billion per month or $19.2 billion per day.

Despite some non-specific talk about “spending cuts,” there seems to be little to no commitment to dealing with the runaway spending in a substantial way.

The Big Beautiful Bill “cut” some spending but increased it in other areas. Furthermore, those “cuts” were from projected spending increases. Actual expenditures will still go up, just not as fast as originally planned. The bottom line is that even with the Big Beautiful Bill, spending will increase on an absolute basis.

And all that waste uncovered by DOGE? Virtually none of it was removed from the budget.

This is par for the course.

You might recall that President Biden promised that the [pretend] spending cuts would save “hundreds of billions” with the debt ceiling deal (aka the [misnamed] Fiscal Responsibility Act).

That never happened.

Supporters of the Big Beautiful Bill expect economic growth stimulated by tax cuts to boost revenue and narrow the deficit. However, history casts significant doubt on this claim.

The ugly truth is the government isn’t committed to cutting spending in any meaningful way, and it always finds new reasons to spend even more, whether for “crises” at home or wars overseas.

The Cost of the Debt

On October 21, the national debt surged to over $38 trillion. Just over one month later, the debt stands at $38.3 trillion.

Uncle Sam must pay interest on all that debt. Interest expense has grown into the second-largest spending category in the federal budget behind only Social Security.

In October, the Treasury forked out $104.4 billion on interest expense alone. That’s a 27.3 percent increase year-on-year.

Interest on the national debt cost $1.2 trillion in fiscal 2025. That was up 7.3 percent over 2024.

Net interest (interest expense – interest receipts) was $91 billion last month.

In the last fiscal year, the federal government spent more on interest on the debt than it did on national defense ($917 billion) or Medicare ($997 billion). The only higher spending category is Social Security ($1.58 trillion).

Much of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and must be replaced by bonds yielding much higher rates. And even after the Federal Reserve cut rates, Treasury yields have pushed upward as demand for U.S. debt sags.

Ramifications

A lot of people act like massive budget deficits don’t matter. However, as the Bipartisan Policy Center points out, the growing national debt and the mounting fiscal irresponsibility make the dollar less and less desirable.

“Confidence in U.S. creditworthiness may be undermined by a rapidly deteriorating fiscal situation, an increasing concern with federal debt set to grow substantially in the coming years.”

This could lead to lower economic growth, higher unemployment, and less investment wealth.

Lack of confidence in the U.S. fiscal situation could also lower demand for U.S. debt. This would force interest rates on U.S. Treasuries even higher to attract investors, exacerbating the interest payment problem.

The bottom line is the U.S. government has a spending problem it won’t address. No matter what the politicians in D.C. claim, there is no way to fix the budget problem by shoveling more money into the hole with tariffs, much less replacing the IRS.

The rest of the world is paying attention.

Biden ran the debt higher at a dizzying pace, but to be fair, this isn’t just a Biden problem. Every president since Calvin Coolidge has left the U.S. with a bigger national debt than when he took office.

It’s going to take more than DOGE rooting out waste to get the borrowing and spending under control. Even if the Trump administration manages to slash discretionary outlays as promised, that only accounts for 27 percent of total spending. The vast majority is for entitlements, and there is little political will to take the scissors to Social Security or Medicare.

And the sad fact is that, given the political incentives, people in power will always kick the debt can down the road. It is a long-term problem that will require painful measures to fix. Politicians don’t want to create pain. That’s a quick path out of office. So, they will punt the debt problem and spend more to make constituents happy.

As I say every month, this is all well and good, but the problem with playing kick the can down the road is that you eventually run out of road.

Read the full article here